Direct Primary Care + The Right Insurance Plan: A 2026 Guide for Maryland, DC, and Virginia Patients

Updated for 2026 insurance rates and IRS Notice 2026-05

When patients first hear about Direct Primary Care, the same two questions come up almost every time. First: “If I’m already paying for health insurance, why would I pay a monthly membership fee for my doctor too?” And right behind it: “Do I have to give up my insurance to join?”

Both are completely fair questions, and the answer to the second one is a clear no. A DPC membership and your health insurance are designed to work together. They cover different things, and together they can cost significantly less than what most patients in Rockville, DC, and Virginia are paying for traditional insurance alone.

This is not a promotional comparison. The three scenarios in this article are built from real 2026 insurance rates specific to the Maryland, DC, and Virginia market, Aurora’s actual published membership fees, and Aurora’s actual lab pricing, all sourced and cited. The numbers show that pairing an Aurora Primary Care membership with the right insurance plan saves patients between $360 and $1,210 per year compared to traditional insurance, depending on age, family situation, and the type of insurance they carry.

You can also explore the numbers interactively in our Cost Comparison Guide →

Here is exactly how it works.

Think of it This Way

DPC and health insurance work together as two separate layers that cover two completely different parts of your healthcare life.

Your Aurora DPC membership is your primary layer

Your membership covers everything that happens between you and Dr. Malhotra, not individual visits, not procedures, not a per-use meter. The monthly fee is what you pay for the ongoing relationship, the access, and the care. Specifically, your membership includes:

- Unlimited primary care visits; no co-pay, no per-visit charge

- Same-day and next-day appointments

- Preventive care, annual wellness visits, and physicals

- Chronic disease management; including diabetes, blood pressure, cholesterol, thyroid conditions, and more

- Acute care for illness and injury

- Mental wellness support within primary care

- Prescription management

- Direct access to Dr. Malhotra by phone, text, and video visit, Dr. Malhotra responds through the Aurora patient app as quickly as possible

- Care coordination and specialist referrals when needed

Your health insurance is your safety net layer

Your membership does not cover specialists, hospitalizations, emergency room visits, or imaging. Those events are exactly what health insurance is designed for, they are unpredictable, high-cost, and thankfully infrequent.

That leaves labs, which sit in a third category. Lab work is not billed through your DPC membership fee, but Aurora members access lab pricing at significantly lower rates than what insurance is typically charged for the same tests. More on that in the lab section below.

The Key Point

DPC and health insurance are not competing options. Removing either one creates a gap.

That is why Aurora does not recommend canceling your insurance when you join.

The 2026 Rule Change That Makes DPC Memberships Tax-Deductible

Starting January 1, 2026, a change that most patients in Rockville have not heard about yet makes Aurora’s membership fee tax-advantaged for the first time. The One Big Beautiful Bill Act (OBBBA), signed into law on July 4, 2025, amended the federal tax code to officially recognize Direct Primary Care arrangements as compatible with Health Savings Accounts (HSAs). The IRS issued Notice 2026-05 in December 2025 to provide implementation guidance.

If you have an HSA, which is typically paired with a High-Deductible Health Plan (HDHP), you can now use pre-tax HSA dollars to pay your Aurora membership fee directly. Aurora’s individual membership starts at $75/month for young adults and $95/month for adults, both well within the IRS limit of $150/month for individuals and $300/month for families.

Here is what that saves in real dollars, depending on your federal income tax bracket:

| Tax bracket | Effective monthly cost after HSA savings |

| 22% (most common in Rockville) | Young adult membership: ~$58/mo · Adult membership: ~$74/mo |

| 24% | Young adult membership: ~$57/mo · Adult membership: ~$73/mo |

| 32% (higher-income households) | Young adult membership: ~$54/mo · Adult membership: ~$70/mo |

Also new in 2026: all Bronze marketplace plans are now HSA-eligible

Under the same legislation, all Bronze and Catastrophic plans sold through ACA marketplaces are now considered HSA-compatible HDHPs, even if they do not meet the traditional HDHP deductible minimums. This is significant for self-employed patients and freelancers in Maryland: a Bronze marketplace plan paired with a DPC membership and an HSA is now a fully legal and tax-advantaged combination. Maryland has the lowest average Bronze plan premiums of any state in 2026, making this combination especially compelling for Rockville and surrounding area patients.

A note on employer health insurance plans

If you have employer health insurance, your company likely offers more than one option. A Standard Employer Plan charges a higher monthly premium in exchange for lower out-of-pocket costs when you use care, predictable co-pays and a lower deductible. A High-Deductible Health Plan (HDHP) charges a lower monthly premium but requires you to pay more before insurance starts covering costs. The trade-off is that an HDHP qualifies you to open a Health Savings Account (HSA), which can be used to pay your DPC membership fee directly, before taxes. Both plan types typically give you access to the same network of doctors and hospitals. The difference is simply in how costs are shared and when.

What These Numbers Look Like for the DC Metropolitan Region

Healthcare costs in the DC metro area are not the same as national averages — and using national averages for this comparison would understate both the problem and the solution. Here is what is specific to this region:

- Maryland has the lowest average Bronze plan premiums of any state in 2026, according to KFF data. This makes the DPC + Bronze HDHP combination unusually favorable for Rockville patients compared to most other states.

- Employer plan premiums in the DC/MD metro area run approximately 20–25% above national averages, reflecting higher provider prices, richer plan designs, and competition from federal employment benefits.

- Lab billing rates in the DC/MD metro area are higher than many markets, meaning Aurora’s deeply discounted lab savings are proportionally larger for local patients.

- Maryland offers a permanent state premium assistance program for residents ages 18–37 that may further reduce marketplace plan premiums for qualifying incomes, making the young adult scenario below even more favorable than shown.

A Real-World Cost Comparison

The following scenarios are built from actual 2026 data for the Rockville and Montgomery County area. Each one compares the total annual cost of traditional insurance options against an Aurora DPC membership paired with the appropriate insurance plan.

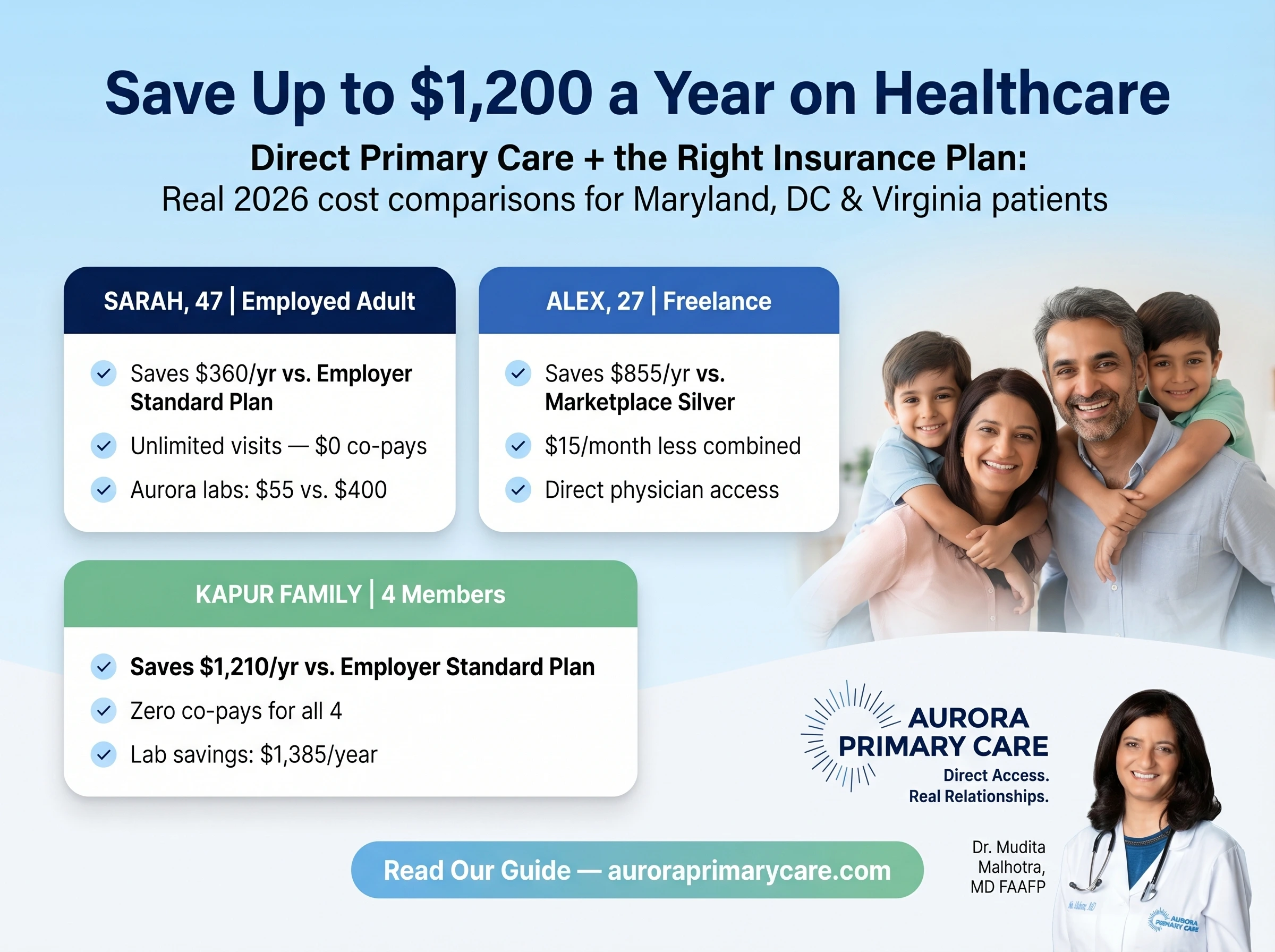

Scenario 1: Sarah, 47 — Employed Adult, Rockville, MD

Sarah works at a mid-size professional services firm in the DC area. Her employer offers both a Standard Plan and an HDHP. She manages borderline cholesterol and blood pressure, sees her doctor five times a year, and has labs drawn twice: a full annual panel plus a mid-year monitoring draw. She may occasionally need an Urgent Care visit.

Aurora membership: Adult rate — $95/month

| Annual cost item | Marketplace Silver (unsubsidized) | Standard Employer Plan (Mont. County) | Aurora DPC + Employer HDHP + HSA |

| Monthly insurance premium (employee share) | $530 | $200 | $160 |

| Monthly Aurora DPC membership | — | — | $95 |

| Combined monthly spend | $530 | $200 | $255 |

| Annual insurance premium | $6,360 | $2,400 | $1,920 |

| Annual Aurora DPC membership | — | — | $1,140 |

| Primary care co-pays (5 visits × $40) | $200 | $200 | $0 |

| Annual labs (annual panel + mid-year monitoring draw) | $400 | $400 | $55 |

| Urgent care visits (1 × $200) | $200 | $200 | $0 |

| Gross annual total | $7,160 | $3,200 | $3,115 |

| HSA pre-tax savings on DPC fee (24% bracket) | — | — | −$275 |

| Net annual total | $7,160 | $3,200 | $2,840 |

| vs. Standard Employer Plan | +$3,960 more | baseline | $360 less |

Aurora saves Sarah $360/year compared to her employer’s Standard Employer Plan, for unlimited visits, zero co-pays, direct physician access by phone, text, and video, and significantly lower lab costs.

At the 32% bracket, HSA savings increase to $365, saving $450 vs. the Standard Employer Plan.

What does this mean in plain language? By switching from the Standard Employer Plan to the HDHP and adding an Aurora membership, Sarah spends $55/month more in combined costs ($255 vs. $200) but eliminates her co-pays, gets same-day access to her physician, and cuts her annual lab costs from $400 to $55. After the HSA tax benefit on her membership fee, she comes out $360 ahead at the end of year — for dramatically better primary care than her Standard Employer Plan.

The DPC+HDHP/HSA combo works especially favorably in the DC/MD/VA region where employer-based health insurance plan costs run consistently 20-25% higher than the national average — with Montgomery County being at the upper end of that range.

Scenario 2: Alex, 27 — Young Adult, Freelance, Rockville, MD

Alex is a 27-year-old freelance designer who purchases his own insurance through the marketplace. He is healthy, sees a doctor about twice a year, but currently has no regular primary care physician and relies on urgent care when he is sick. He recently aged off his parents’ insurance plan and is comparing his marketplace options.

Aurora membership: Young adult rate — $75/month

| Annual cost item | Marketplace Silver (unsubsidized) | Aurora DPC + Marketplace Bronze HDHP + HSA |

| Monthly insurance premium | $345 | $255 (Bronze HDHP) |

| Monthly Aurora DPC membership | — | $75 |

| Combined monthly spend | $345 | $330 |

| Annual insurance premium | $4,140 | $3,060 |

| Annual Aurora DPC membership | — | $900 |

| Primary care co-pays (2 visits × $35) | $70 | $0 |

| Annual labs (standard annual panel) | $240 | $35 |

| Urgent care visits (1 × $200) | $200 | $0 |

| Gross annual total | $4,650 | $3,995 |

| HSA pre-tax savings on DPC fee (22% bracket) | — | −$200 |

| Net annual total | $4,650 | $3,795 |

| vs. marketplace Silver | baseline | $855 less |

Aurora saves Alex $855/year compared to a marketplace Silver plan, while also costing $15 less per month ($330 vs. $345 combined monthly).

At the 24% bracket, HSA savings increase to $215, saving $870 vs. Silver. Maryland’s Bronze premiums are the lowest of any state in 2026, this combination is especially strong for Rockville patients.

A Bronze HDHP plus an Aurora Young Adult membership costs less per month than a Silver plan alone — $330 vs. $345. And over a full year, Alex saves $855 because he eliminates co-pays, eliminates an urgent care visit that his direct physician access prevents, and pays significantly less for annual labs. He also gains something a Silver plan cannot provide: a physician who knows him, responds to his messages, and is available when he gets sick.

Maryland also offers a permanent state premium assistance program for ages 18–37 that may further reduce net premiums for qualifying income levels.

The gap widens for patients with chronic conditions who need to see their doctor more frequently or require more regular labs. Families also fare better with the Aurora TogetherCare membership providing a discounted rate for teens enrolled with an adult or young adult member.

Scenario 3: The Kapur Family — Rockville, MD

Two parents (both 47), a 23-year-old on the family membership and an 18-year-old. Parents employed at a DC-area firm. Mr. Kapur manages diabetes and Mrs. Kapur has borderline cholesterol and blood pressure. Approximately 15 primary care visits across the family receiving annual panels plus quarterly monitoring draws for Mr. Kapur and a mid-year monitoring draw for Mrs. Kapur.

Aurora membership: 2× Adult ($95) + Young adult ($75) + Teen family rate ($35) = $300/month

| Annual cost item | Marketplace Silver (family, unsubsidized) | Standard Employer Plan (Mont. County) | Aurora DPC + Employer Family HDHP + HSA |

| Monthly insurance premium (family) | $1,570 | $710 | $580 (HDHP) |

| Monthly Aurora DPC (4 members) | — | — | $300 |

| Combined monthly spend | $1,570 | $710 | $880 |

| Annual insurance premium | $18,840 | $8,520 | $6,960 |

| Annual Aurora DPC (all 4 members) | — | — | $3,600 |

| Primary care co-pays (15 visits × $40) | $600 | $600 | $0 |

| Annual labs (all 4 members) | $1,600 | $1,600 | $215 |

| Urgent care visits (2 × $200) | $400 | $400 | $0 |

| Gross annual total | $21,440 | $11,120 | $10,775 |

| HSA pre-tax savings on DPC fee (24% bracket) | — | — | −$865 |

| Net annual total | $21,440 | $11,120 | $9,910 |

| vs. Standard Employer Plan | +$10,320 more | baseline | $1,210 less |

An Aurora TogetherCare membership saves the Kapur family $1,210/year compared to the Standard Employer Plan, for unlimited primary care for all four members, zero co-pays, and dramatically lower lab costs, including quarterly diabetes monitoring.

At the 32% bracket, HSA savings increase to $1,152, saving $1,497 vs. the Standard Employer Plan. Families managing chronic conditions see the largest savings from Aurora’s deeply discounted lab pricing.

What does this mean in plain language? The family pays $880/month combined (HDHP + Aurora) versus $710/month for the Standard Employer Plan alone — $170 more per month. But they eliminate $600 in annual co-pays, $400 in urgent care visits, and $1,385 in lab costs. After the HSA tax benefit on their DPC fees, they come out $1,210 ahead at year end — for four people’s unlimited primary care access, including Mr. Kapur’s full quarterly diabetes monitoring program.

The teen family rate is worth noting specifically. The Kapur’s 18-year-old gets complete primary care — sports physicals, acute illness visits, mental health support, vaccination guidance and acne treatment — for $35/month as a family rate, versus $55/month as an individual enrollment. That rate applies to any enrolled teen when an Adult or Young Adult member is enrolled and takes responsibility for payments and treatment follow-up.

A word on Mr. Kapur’s HDHP deductible and diabetes

With Aurora managing Mr. Kapur’s diabetes through primary care — quarterly monitoring, prescription management, and direct physician access — his care stays within the DPC relationship in a well-managed year and does not trigger the HDHP deductible at all.

That said, diabetes does carry a higher probability of specialist involvement than most conditions. An endocrinologist if blood sugar control becomes difficult, an ophthalmologist for an annual diabetic eye exam, a podiatrist. If Mr. Kapur sees two specialists in a year, he might spend $500–$900 toward his $3,000 individual deductible. He is unlikely to reach it, but it is worth knowing it is there.

If a more serious event occurs — a cardiac episode, a hospitalization — costs could reach and exceed the deductible. At that point his HDHP insurance begins paying its share, which is exactly the protection it was designed to provide.

The deductible is not something to ignore. It is something to plan for, which is exactly what the HDHP and HSA combination is designed to help you do.

What About Lab Work and Testing?

This is where DPC delivers one of its most underappreciated benefits.

At Aurora Primary Care, members don’t pay standard insurance-billed lab rates. We work with partner labs to offer you deeply discounted pricing — often 60–85% less than what insurance is billed for the same test.

How it works in practice:

- Routine blood panel — typically $8–$15 at member rates vs. $150+ billed to insurance

- Thyroid panel — typically $10–$25 vs. $100–$200 billed to insurance

- Allergy testing (blood-based) — significantly reduced vs. specialist billing

If you have insurance with lab coverage, Dr. Malhotra can route lab orders through your insurance. If your deductible is high or you prefer the predictability, the member lab rate is often simply cheaper. For a patient like Mr. Kapur, who requires quarterly monitoring, this translates to $630 per year in lab savings alone.

The Best Health Insurance to Pair with a DPC Membership

Not every insurance plan pairs with DPC in the same way. Here is how the most common options work for patients in Maryland, DC, and Virginia.

High-Deductible Health Plan (HDHP) — the best pairing for most patients

HDHPs carry lower monthly premiums but higher deductibles. On their own, they can feel risky — routine care before the deductible is met costs full price. Paired with a DPC membership, that concern largely disappears. Aurora handles all primary care, so patients rarely trigger the deductible for everyday health needs. The HDHP provides catastrophic protection at a lower monthly cost, and the HSA provides a tax-advantaged way to pay the DPC membership fee. For 2026, all Bronze and Catastrophic marketplace plans are HSA-eligible — a new benefit that makes this pairing available to more patients than ever before. Want to see what DPC costs for your specific situation? Use our interactive cost comparison guide →

Standard Employer Plan — works alongside DPC independently

If you have a Standard Employer Plan, you keep it exactly as it is. Your Aurora membership operates independently — no insurance billing is involved. You use your membership for all primary care and your Standard Employer Plan for specialist referrals, hospital care, and anything outside primary care. If your employer also offers an HDHP option, it is worth running the numbers: for most Montgomery County patients, switching to the HDHP and enrolling in Aurora results in meaningful net annual savings versus staying on the Employer Plan alone.

Medicare and Medicaid — can coexist with DPC

Patients on Medicare or Medicaid can enroll in a DPC membership. Medicare continues to cover specialist visits, hospitalizations, imaging, and emergency care. Your DPC membership covers your primary care relationship outside of Medicare billing — the two do not conflict. Dr. Malhotra is not currently accepting Medicare patients, but a waitlist is open and enrollment is expected to begin in the coming months.

No insurance — DPC as a primary care foundation

If you currently have no insurance or a plan with costs so high that routine care feels out of reach, an Aurora DPC membership provides meaningful, predictable access to a personal physician for a flat monthly fee — with no per-visit charges and deeply discounted lab pricing.

An Aurora membership is not insurance and cannot replace it. If you have insurance, you will use it for hospitalizations, specialist care, and emergencies. If not, a DPC membership provides immediate stability for everyday primary care needs.

Three Things to Do Right Now

- Figure out which scenario above most closely matches your situation. Are you self-employed and buying your own insurance? Do you have employer coverage? Are you insuring a family? The right financial case for Aurora looks different depending on where you start.

- Pull your actual healthcare spending from last year. Add up everything you actually paid: premiums, co-pays, urgent care visits, lab fees, and any out-of-pocket costs before your deductible was met. Most patients who do this are surprised by the total. Compare that number against the relevant scenario above.

- Use our Interactive Cost Guide to run the comparison for your situation.

- Schedule a Free Meet & Greet with Dr. Malhotra. This is not a sales call. It is a no-commitment conversation about your health, your current coverage, and whether Aurora’s model makes sense for your specific situation.

The Bigger Picture

Healthcare in the United States was designed around insurance billing — not around the patient-doctor relationship. That system works reasonably well for complex, unpredictable, high-cost events. It works poorly for the everyday, relationship-based, preventive care that keeps people well year after year.

Direct Primary Care separates those two layers intentionally — and puts each one where it belongs. Your insurance protects you from the unpredictable. Your DPC membership takes care of everything in between — the visits, the conversations, the follow-ups, the adjustments, the relationship with a doctor who actually knows you.

That’s not a workaround. That’s how primary care was always supposed to work.

And it matters financially — as the three scenarios above demonstrate.

It also matters in ways that are harder to put in a table:

- When your doctor knows your history, you get better care faster.

- When visits have no additional cost, you stop postponing care until things get worse.

- When labs are affordable, you actually get the testing and monitoring you need.

- When you can send a message to your physician and receive a timely response, urgent care visits become far less necessary.

- When your insurance premium is lower, your monthly budget has room to breathe.

The goal isn’t to game the system. The goal is to actually have access to a doctor — reliably, affordably, and without administrative friction every single time you need one.

If you’ve been carrying insurance but quietly avoiding using it because every visit still costs money out of pocket, Aurora Primary Care was built specifically for that situation.

And in Maryland, where Bronze HDHP premiums are the lowest of any state in 2026 and the new HSA rule makes your membership fee tax-deductible, the conditions for making this model work have never been better.

We offer a Free Meet & Greet with Dr. Malhotra — no commitment, no paperwork, no pressure. A real conversation about your health, your coverage, and whether Aurora is right for you.

Frequently Asked Questions

1. Do I have to cancel my health insurance to join Aurora?

No — and we strongly advise against it. Your Aurora DPC membership covers your primary care relationship. Health insurance is still essential for specialist visits, hospitalizations, and emergency care. The two are designed to work alongside each other, not replace one another.

2. How does a DPC membership work with my employer-provided insurance?

Your Aurora membership operates completely independently of any insurance billing. You use the membership for all primary care and your employer plan for specialist referrals, hospital care, and anything outside primary care. If your employer offers both a Standard Employer Plan and an HDHP option, it is worth comparing them. For most Montgomery County patients, switching to the HDHP and enrolling in Aurora produces net annual savings versus staying on the Standard Employer Plan.

3. Can I use my HSA to pay for a DPC membership in 2026?

Yes. Starting January 1, 2026, the One Big Beautiful Bill Act (IRS Notice 2026-05) classified DPC membership fees as qualified HSA expenses. You can use pre-tax HSA dollars to pay your Aurora membership fee, up to $150/month for individuals and $300/month for families. Aurora’s membership fees fall well within those limits. The tax savings range from approximately $200 to $365 per year depending on your tax bracket.

4. Does my DPC membership fee count toward my HDHP deductible?

No. Under IRS Notice 2026-05, DPC membership fees explicitly do not count toward your HDHP’s annual deductible or out-of-pocket maximum. Your catastrophic coverage safety net is fully intact.

5. Why is an HDHP the best insurance to pair with DPC?

HDHPs have lower monthly premiums than Standard Employer Plans but higher deductibles. Without reliable primary care access, that deductible exposure feels risky. With Aurora, virtually all your primary care needs are covered by your membership, so you are unlikely to trigger that deductible from everyday health concerns. The net result: lower insurance premiums, lower combined annual spend, and HSA-compatible tax savings.

6. What does Aurora’s membership cover that insurance typically does not?

Your membership includes unlimited primary care visits with no per-visit charge, same-day and next-day appointments, direct access to Dr. Malhotra by phone, text, and video visit, chronic disease management, preventive care, acute illness care, mental wellness support, and care coordination. Most insurance plans charge a co-pay for each visit and offer no direct access to a physician between appointments.

7. Does Aurora cover lab work?

Lab work is not billed through your membership fee. Aurora members access deeply discounted lab pricing — typically 60-85% lower than standard insurance billing rates for the same tests. If your insurance covers labs and that is the more cost-effective path, Dr. Malhotra can route orders through your insurance instead.

8. How quickly will Dr. Malhotra respond to my messages?

Dr. Malhotra responds to messages sent through the Aurora patient app as quickly as possible. During non-working hours or while she is seeing patients, there may be a delay — but you will receive a timely, direct reply from your physician, not a portal message routed through a nurse or answering service.

9. What does the teen membership include?

Aurora’s teen membership (ages 12–19) covers sports and school physicals, acute illness care, mental wellness support, vaccine guidance and management, acne and other common dermatological concerns within primary care, and routine health counseling. Standard diagnostic lab panels begin at age 18; Dr. Malhotra orders labs for teen members under 18 when clinically indicated.

10. Who qualifies for the teen caregiver family rate of $35/month?

The $35/month teen rate is available when a caregiver Adult or Young Adult member is enrolled in the Aurora TogetherCare membership and takes responsibility for the teen’s payments and treatment follow-up. There is no specific relationship requirement — the caregiver does not need to be a parent or legal guardian — but they do take on formal responsibility for the teen’s care coordination within the practice.

11. Does Aurora offer video visits?

Yes. Dr. Malhotra is available by phone, text, and video visit for appropriate clinical situations alongside in-person appointments.

12. Can I use DPC if I have Medicare or Medicaid?

Yes. Patients on Medicare or Medicaid can enroll in a DPC membership. Medicare continues to cover specialist visits, hospitalizations, imaging, and emergency care. Dr. Malhotra is not currently accepting Medicare patients, but a waitlist is open and enrollment is expected to begin in the coming months.

13. What happens when I need a specialist?

Dr. Malhotra coordinates specialist referrals directly — with more clinical context and communication than is typical in a standard insurance-based practice. Your specialist visit is then handled through your health insurance exactly as it would be without a DPC membership. Better-managed primary care tends to reduce the frequency of unnecessary specialist referrals, because your primary care physician knows your full picture before making one.

14. Is a DPC membership considered health insurance?

No. A DPC membership is not health insurance and does not satisfy any health insurance requirement. It is a direct healthcare service agreement between you and your physician. You still need health insurance for specialist care, hospitalizations, emergency care, although Dr. Malhotra can guide you towards cash-pay imaging options.

15. What is Aurora’s membership pricing?

Teen (ages 12–19): $55/month individual or $35/month caregiver rate in Aurora TogetherCare. Young Adult (ages 20–29): $75/month. Adult (ages 30–64): $95/month. No enrollment fees, no per-visit charges, no hidden costs. Visit the Aurora membership page for full details or schedule a Free Meet & Greet to ask Dr. Malhotra directly.

16. Can I join mid-year if I already have an insurance plan?

Yes. You can enroll in Aurora’s DPC membership at any time — it is completely independent of your insurance plan’s enrollment period. Your insurance remains unchanged, and your Aurora membership begins immediately upon enrollment.

A Note on The Comparisons

The cost comparisons in this article use real 2026 insurance market data for the Rockville and Montgomery County area, Aurora’s actual membership fees, and Aurora’s actual lab pricing. They are built to reflect realistic situations for patients in this region — not best-case scenarios. All sources are cited below.

These comparisons are starting points for your own thinking, not personalized financial quotes. Your actual costs will depend on your specific insurance plan, your employer’s contribution structure, your age, your location, and how much healthcare you use in a given year. Before making any changes to your health coverage, review your own plan documents and make the decision that is right for your situation. Aurora Primary Care is a medical practice, not a licensed insurance broker or financial advisor.

Sources

IRS Notice 2026-05 (DPC and HSA eligibility guidance)

IRS Newsroom — Treasury/IRS guidance on OBBBA HSA changes

KFF 2025 Employer Health Benefits Survey (premiums, employee contributions, HDHP data)

KFF 2025 Annual Family Premiums Survey

KFF — Policy Changes and High-Deductible Health Plans 2026 (Bronze plan HSA eligibility)

KFF Health Insurance Marketplace Calculator (age-rated premium benchmarks by state)

Mercer 2025 National Survey of Employer-Sponsored Health Plans

Maryland Insurance Administration — 2026 ACA Approved Rates

ValuePenguin — 2026 Maryland Health Insurance Analysis

Salusion — Maryland Health Insurance Snapshot (Montgomery County premiums by age)

Becker’s Payer Issues — States Ranked by Average Lowest-Cost ACA Bronze Premiums 2026

DC DISB — 2026 Individual Health Insurance Rate Approval

HealthInsurance.org — Maryland Health Insurance Marketplace 2026 ACA Guide

HealthEquity — Key Changes to HSAs and HRAs in 2026

Maryland Health Connection — Maryland Premium Assistance Program

Lab pricing reflects Aurora’s current pricing and is subject to change. Pricing varies by test and is significantly lower than standard insurance billing rates across Aurora’s full test menu.

Dr. Mudita Malhotra, MD, FAAFP, is the founder of Aurora Primary Care in Rockville, MD — a Direct Primary Care practice dedicated to accessible, affordable, and relationship-based primary care for individuals and families in Maryland, DC, and Virginia. Schedule a Free Meet & Greet to speak with Dr. Malhotra directly about your healthcare situation.